Sale and Unitrust

Are your appreciated assets, such as stock, bonds or real estate, producing little or no income?

If you sell your appreciated assets, you will pay a large capital gains tax. A sale and charitable remainder unitrust may be the solution to avoid capital gains tax.

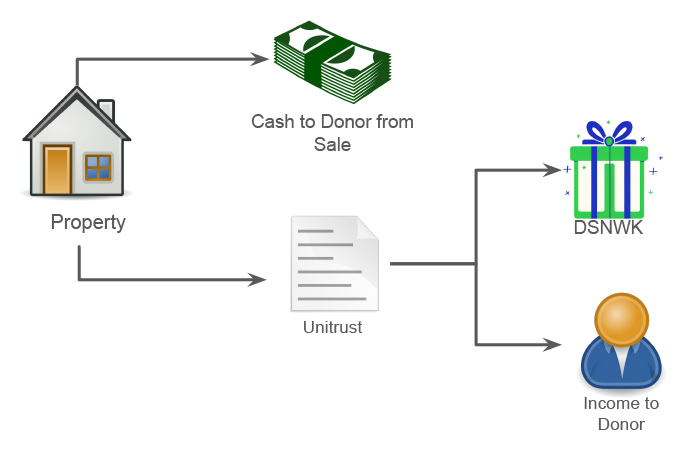

Flowchart: Donor transfers an undivided portion of property to a unitrust. When property is sold, the donor and the unitrust receive cash from the sale. The donor receives payouts from the unitrust and the DSNWK receives the remainder at the end of the trust term.

Benefits of a sale and unitrust

- Receive cash from the sale. You can use this cash to purchase another residence, to save for retirement, to travel, to meet your daily needs or to meet some other financial goal

- Receive income from the unitrust for the rest of your life and future retirement

- Obtain an income tax deduction that may reduce your tax bill this year

- Further the work of Developmental Services of Northwest Kansas with your gift

How a sale and unitrust works

- You establish a charitable remainder unitrust and transfer a portion of your assets to the trust.

- The assets are then sold. You receive cash from the sale, and the rest of the sale's proceeds are paid to the charitable unitrust.

- The trust will provide you with income for the rest of your life.

- You receive a charitable deduction this year to offset your tax on the cash proceeds that you receive from the sale.

More on sale and unitrust

When transferring a portion of your primary residence to fund a unitrust, you may apply your one-time home exclusion to reduce or eliminate capital gains tax that would otherwise be due from the sale. Your tax advisor can assist you to determine if you should utilize this strategy.

Contact us

If you have any questions about a sale and unitrust, please contact us. We would be happy to assist you and answer any questions you might have.